Sometimes while working at a PPC Agency, we tend to forget the bigger picture of our clients’ businesses. The beginning of a client/agency relationship often follows this process:

- Introduction and familiarization with the paid search accounts

- Nailing down a paid search goal(s)

- Understanding the business as a whole and how PPC fits in

This process is a great start, but we need to go further.

To develop a greater sense of what is going on in their industry or business, think about the economic factors surrounding the company. When applying basic economics principles while gauging performance, we can make sure our paid search strategy is in line with what’s going on both within the business and the industry.

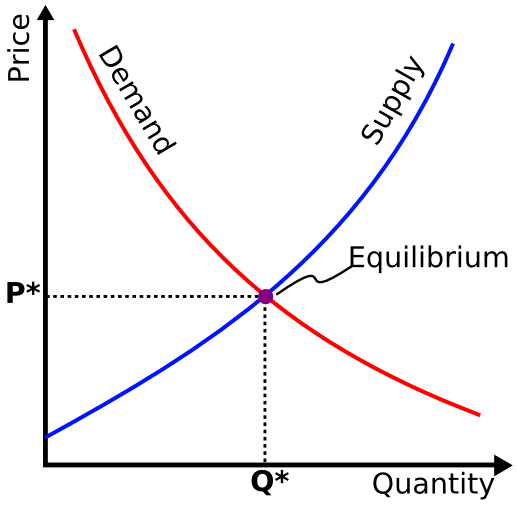

Supply & Demand

This principle is basic, and it’s pretty much the first thing you learn in any Econ-101 class. Here is the overview.

Supply

The law of supply says that, all other things remaining equal, as the price of a good increases (decreases), the quantity of that good supplied will increase (decrease).

Factors impacting supply include:

- Cost

- Government policies

- Weather or climate

- Prices of substitute goods

- Number of producers

Demand

The law of demand states that, all other things remaining equal, as the price of a good increases (decreases), the quantity of that good demanded will decrease (increase).

Factors impacting demand include:

- Consumer income

- Consumer preferences

- Complimentary goods

- Advertising

- Expectations

- Market demographics

Why Supply & Demand Is Important In PPC

There are two main ways that shifts in supply or demand can affect you as a PPC account manager: 1) goals can change, or 2) performance can change based on the outside factors listed above.

Regarding point number one, it’s important to have discussions about external forces that impact overall marketing goals. Say your client can produce less of their product because taxes were recently raised. That’s important for you to know, because it affects their bottom line and profitability (ex: ROAS goals may shift).

For point number two, if you see an unexpected drop in performance and can’t find any reasonable explanation, think about what could be happening in the industry to impact demand. Say you see a huge impression decline for your branded campaigns. It could be that a competitor was recently in the news or significantly lowered prices.

Marginal Cost & Marginal Benefit

This topic can be prudent when a client wants to know whether they should increase PPC budgets.

Marginal cost refers to the opportunity cost of producing one additional unit of a good (in this case, the added cost of getting one more conversion). Marginal benefit refers to the increase in utility of one more good or service (in this case, what’s gained from that extra conversion).

Another key theory that goes hand in hand with marginal cost & benefit is the law of diminishing marginal returns. This law states, “as the amount of any one input is increased, holding all other inputs constant, the amount that output increases for each additional unit of the expanding input will generally decrease.”

Importance To PPC

Let’s say a client of yours is spending $10,000 monthly and wants to increase budget by $20,000 for next month. While this initially sounds great and your client is expecting to reap the benefits of loads more conversions, it’s important to understand that this may not be the case.

While you’re ramping up spend, those extra dollars likely aren’t being used in the most efficient way possible. These inefficiencies lead to less value per dollar, as each dollar spent leads to fewer conversions. While you might be able to spend that extra $20k, you’re not likely to see an equal 200% increase in conversions. Of course you can optimize that extra spend along the way to get the most bang for your buck, but it’s not likely to be perfectly efficient right away.

Profit Margins & Loss Leaders

Profit margin is often referred to in the PPC world as return on ad spend (ROAS). This number portrays how much money the company is earning for every dollar spent. Typically we want to see a ROAS of greater than 100%, meaning for every dollar spent the company earns more than $1.

Loss leaders are products that a business is okay with losing a bit of money on, as they are shown to bring in new customers or be associated with a higher average order value.

Why It’s Important In PPC

For eCommerce accounts we are given an overall ROAS goal. While this goal is perfectly fine to optimize towards, we can have a bigger impact on the client’s business if we understand which products lead to more revenue (even if the product by itself isn’t making money).

For example, say you’ve got an account that sells a subscription service. For one particular subscription you notice that you only have a ROAS of 20%. Instead of pulling back on those campaigns, find out from your client if people who bought this subscription are much more likely to come back and become a repeat customer. By having these types of conversations with your client and being aware of their business model, you can help them generate more long-term revenue.

In a similar vein, knowing the profit margins for each product is helpful when determining PPC goals and optimizing towards them. Let’s look at an example.

Your client sells tennis balls. Each tennis ball costs $20 to produce, and sells for $25 ($5 profit margin). Now in AdWords you spent $50 on the tennis ball campaign and sold 5 ($125 in revenue, 250% ROAS, $10 CPA). This looks great, right? Well when you factor in the production costs you get a total cost of $150. With $125 in revenue, this isn’t looking so awesome anymore. In this example you would have to sell 10 tennis balls at that level of spend to break even.

Closing Thoughts

Hopefully thinking about your client’s business will drive conversations about goals and strategy. Really becoming familiar and knowing what’s going on in your client’s business and industry will help you form a collaborative relationship in which you can really contribute to business growth. While some of these ideas and theories don’t necessarily come with direct action items, it’s important to think about and be aware of.